Concerning various methods of company valuation

It’s the major question for founders, shareholders, and investors: How much is a company really worth? The answer to this question depends on whether you are the entrepreneur who wants to make as much profit from the sale of company shares as possible, or if you are the investor who wants to participate in a company at the most affordable conditions possible.

There is no true company value. This is also the reason why this topic usually gets people riled up. The company valuation is no objective value; it is always within the scope of discretion. Particularly in the field of venture capital, which deals with very young companies without a history of reliable values, it is not always easy to determine a company’s value.

Even experienced appraisers can reach sales price deviations of more than 50% by using different processes for company evaluations. The different processes to determine the company value thus represents a bandwidth rather than a specific value. It aims to rationalize a usually emotional process.

The investor legend Warren Buffet once said about company valuations: “The price is what you pay. The value is what you receive.” The value describes the use that an economic good (the company) has for the prospective buyer. The price, on the other hand, is the result of negotiations in which both the buyer and seller try to reach a result that best suits their interests. As such, the company value listed on Companisto is a price for investors, since it is the result of a negotiation process.

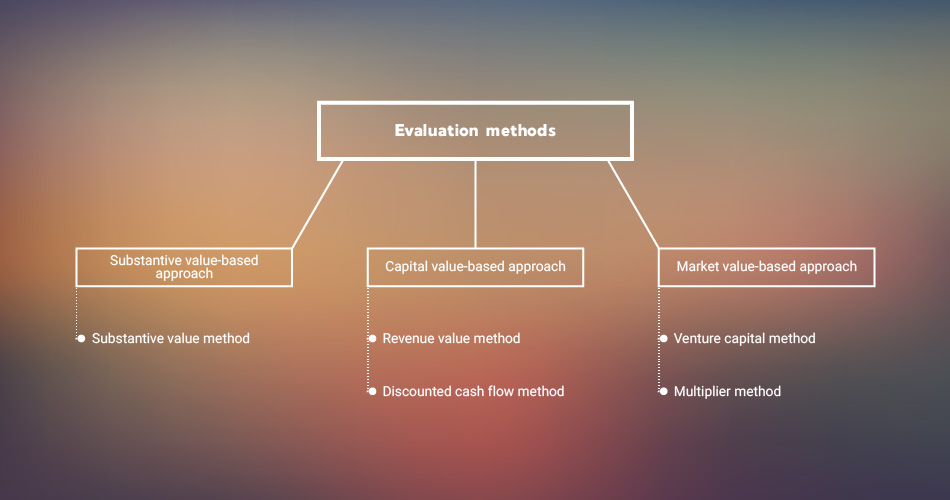

Classic methods of company valuation

In the past, companies in Germany were valued exclusively on the basis of past earnings (after tax). The 60s saw the introduction of the intrinsic value method, soon followed by the Stuttgart procedure. The capitalized earnings method has gained importance since the 80s.

It was not until the 90s that methods from the English-speaking realm made their way to company evaluations in Germany. This included especially the discounted cash flow method, the multiplier procedure, and the venture capital method. This completed a shift away from evaluating companies based on past earnings toward evaluations of future (and thus uncertain) income.

Until 2000, the Institute of Auditors (IDW), which sets the standards for company valuation in Germany, only recognized the capitalized earnings method. Nonetheless, the rising number of transnational company sales and mergers, particularly between German and Anglo-Saxon companies, has brought about increased acceptance of the discounted cash flow method, which since is considered equal to the capitalized earnings method. You will find an overview of classic evaluation methods below.

Substantive value method

The substantive value method calculates the value that the buyer would have to reach in order to reproduce the entire company. All available assets are determined in order to calculate the net asset value. First, all material goods (inventory, fleet, machinery, buildings, technology, etc.) are listed in an inventory. The individual components of the company’s assets are evaluated according to their replacement cost.

Next, all current company liabilities are deducted from the company assets. The result is the partial reproduction value. However, the inventory does not contain immaterial goods (customer base, delivery network, brand name, image, know-how, etc.), all of which also influence the company value. Their value has to be estimated, as there are no recognized methods to calculate them. The total reproduction value is reached by adding the immaterial goods to the partial reproduction value.

One advantage of the substantive value method is that no forecasts are necessary. It is thus very easy to apply. However, it also has considerable disadvantages. Material goods are evaluated individually and not as a whole although it is precisely the interplay of the individual components that make up a successful company.

The profitability of a company does not flow into the company valuation at all. Another weakness of this method is the estimation of immaterial goods. This can warp the company value considerably. As a result, this method is rarely used for evaluation, for example, if an enterprise has a very high proportion of fixed assets and only a few intangible assets.

Revenue Value Method

The revenue value method is a wide-spread means of company evaluation. It assumes that the value of a company can be found in its potential to generate future profits. The buyer is primarily interested in finding out how long the acquired company will take to earn the purchase price. Future profits thus play a more important role than past income.

The calculations are based on a predicted income statement. The value of the equity capital of a certain point in the future is calculated by discounting the future income surpluses. Discounting is a calculation that determines the current cash value of a future payment. When calculating the revenue value, one takes into consideration that the buyer has to pay not only for investments in the company from future profits but also for interest and loan repayments in financing the purchase price.

The question the investor must answer is whether or not his or her capital is better invested in the company or in other assets. Therefore, he or she compares the interest rate from potential future company revenue with the return achievable through alternate investments (also known as the capitalization rate). In most cases, one looks at a span of three years. The results for each year are aggregated, giving the investor the company’s revenue value. The formula is:

RV = ∑ S t / (1 + r) t

RV = Revenue value

S = Distributed income surplus

r = Capitalization interest rate

t = Time period

The revenue value is the difference between the future income surplus and the so-called capitalization interest rate. The capitalization interest rate, in turn, is comprised of the basic interest and risk premium. Mathematically speaking, a high capitalization interest rate under the fraction line reduces revenue surpluses above the fraction line more than a small value does.

The revenue value method differentiates between an objective and a subjective revenue value. During the forecasting of the company’s future successes, the objective revenue value assumes that the company will operate the same as before and that the market develops realistically. The subjective revenue value on the other hand also considers future measures (investments, restructuring, synergy effects, etc.) that can positively influence the company’s success.

A major challenge to the revenue value method is that it is strongly dependent on the capitalization interest rate. Since it has a great impact on the company value, this rate has to be carefully calculated. In any case, the revenue value is a value of orientation that can serve as a solid basis for company valuation negotiations. Buyers and sellers can use this basis to determine upper and lower value limits and to find a common price.

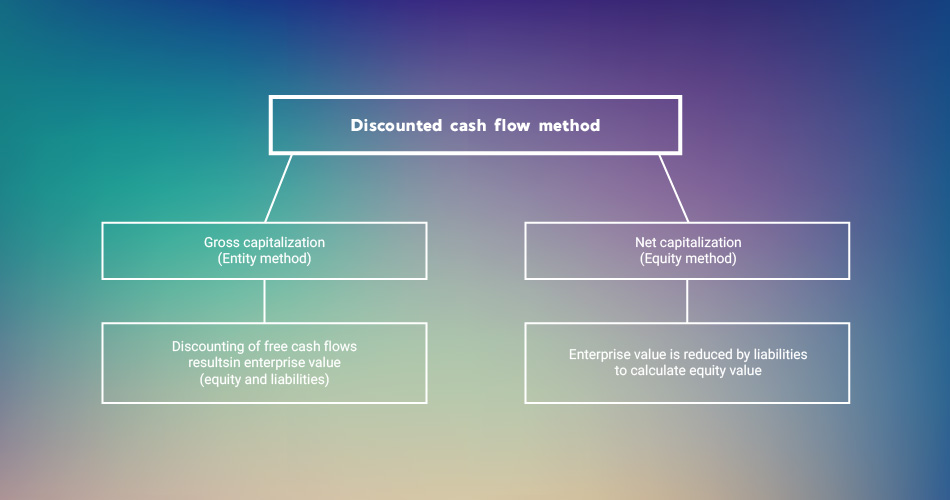

Discounted cash flow method

The discounted cash flow (DCF) method, also known as capital value method in Germany, is the most known method of company evaluation worldwide. It is based on the discounting of forecasted free cash flows that can be distributed to shareholders.

Detailed planning figures are necessary to determine free cash flow. The time period should cover the next three to five years. The most important financial figures to determine future cash flows are the projected income statements and balance sheets for the next years, working capital, and resource and personnel planning. Ideally, the operating results of the past three years are also available as assessment basis.

The determined free cash flows are then discounted using the discount rate (similar to the capitalization interest rate). Like the capitalization interest rate, the discount rate includes the so-called cost of capital. The discount rate is derived from comparative market figures (e.g.: Dax performance, bond yield, etc.) and also includes a risk premium (market risk, beta factor, etc.).

The cost of capital represents the return from comparable investments in other assets that the investor misses out on due to investing his or her capital in the company. The forecasted cash flows of the next years are reduced by the cost of capital since the investor could generate this capital if he or she did not place the available capital into the company. The DCF method thus follows the same approach as the German revenue value method.

The DCF method distinguishes between two approaches: gross capitalization (entity method) and net capitalization (equity method). The entity method calculates the company value in two steps. First, one determines the enterprise value by discounting the plan years’ predicted free cash flows. The enterprise value does not differentiate between equity and liabilities.

The second step in the entity method is the termination of the equity value. To do so, one subtracts the value of liabilities from the enterprise value. Liabilities represent that part of the company's capital which the company has borrowed against interest from outside creditors, i. e. which was not invested in the company by the shareholders.

The most wide-spread approaches of the entity method are the weighted average cost of capital (WACC), the adjusted present value (APV), and the total cash flow (TCF).

The calculation of the company value in the equity method requires only one step. The cash flows attributable to equity owners are discounted to the valuation date using the capitalization interest rate. The capitalization represents the return that the equity owner could generate through an alternative investment with similar risk. The equity method is thus equivalent to the German revenue value method.

The advantage of the DCF method is that cash flows are less likely to be warped by accounting policies and are thus more expressive of a company’s earning power. This reduces the likelihood of erroneous evaluation and so-called “window dressing.” The term “window dressing” refers to accounting measures that visually improve the balance sheet as part of a financing round for investors without sustainably improving the balance sheet structure.

Beyond this, the DCF method offers advantages in the determination of future liquidity and potential risks, since it takes detailed information about the origin and use of cash flows in operative business into consideration. One of its disadvantages, however, is that there is no universally applicable definition of which free cash flows are to be discounted using the capitalization interest rate. Furthermore, the challenge to calculate an especially conclusive capitalization interest rate remains.

Company valuation in venture capital

Startups are young companies with an innovative business idea who have limited seed capital but great potential for growth. These companies are characterized by a great dynamic but also great uncertainty. They frequently concentrate large portions of their funds in immaterial assets.

Startups generally go through four phases: a seed phase, a startup phase, a growth phase, and a maturing phase. In the first two phases, cash flow tends to be negative, since the company development needs to be invested in first. A positive cash flow can be expected only from the growth phase onward.

From that point onward, the revenue value and the DCF method are suitable to determine the company’s value. However, two other methods lend themselves better to company valuation during the seed and start-up phase, according to the auditing firm Ernst & Young: the venture capital and the multiplier method.

Multiplier method

Using the multiplier method, the company’s value is derived from ratio indicators, so-called multipliers. The multiplier indicates the relationship between the realized market value (sales price of an equivalent enterprise) and the chosen company identification number (revenue or profit). The value of the company is thus compared to similar companies, which makes this method particularly practical.

In the first step, one starts with a company analysis. Included in this analysis are the current and forecasted key financial figures such as customer or user number, revenue per employee, and future cash flows. Next, one evaluates the potential for success through a strategic analysis. Finally, one decides on parameters to determine company value. In the second step, one selects a suitable multiplier. The multiplier is named after the company identification number it relates to (e.g.: revenue, EBIT, or EBITDA multiplier). There are three categories of multipliers:

- Equity multiplier (price-earnings ratio, price/book value ratio, price-cash flow ratio)

- Entity multiplier: enterprise value / revenue, enterprise value / EBIT, enterprise value / EBITDA, enterprise value / free cash flow

- Special multiplier: operative key figures, variations and combinations of classic multipliers (e.g.: sales and EBIT multiples in relation to company growth)

The third step entails selecting a reference group. The reference group should consist of companies that are comparable in size and industry and who have a similar reason for valuation (e.g. upcoming financing round). The company value is calculated on this basis while keeping in consideration the company’s individual strengths and weaknesses and making adjustments accordingly.

Example: A startup from the hardware sector records revenue of EUR 2,000,000 in its financial figures (balance sheet, income statement). In order to determine the company value, one looks at the sales prices of hardware startups with comparable revenue and calculates the average. In doing so, one discovers that hardware startups have an average revenue multiplier of 0.55. Thus, we calculate our startup’s company value as follows:

Revenue x revenue multiplier = company value

EUR 2,000,000 x 0.55 = EUR 1,100,000

The multiplier method is easy to use since it only requires revenue or profit and the respective multiplier. It can also be used in the case of missing revenue figures and unprofitable companies and is therefore also suitable for early-stage valuation. In addition, balance sheet policies, i.e. short-term measures to influence the balance sheet, only have a minor impact on the result.

The disadvantage of this method is that it considers neither the company’s profitability nor its earning power. It also doesn’t consider the potential for growth. For small enterprises (e. g. artisan enterprises), there is the additional problem that there are only a few publicly accessible databases on corporate transactions. As a result, the amount of data is often insufficient to determine meaningful multipliers.

Venture Capital Method

The venture capital method (VC method) combines the multiplier and DCF methods. It is a useful method for company valuation before the entry of an investor or a VC company (pre-money valuation). According to Ernst & Young, more than half of all VC companies use this method, making it the most frequently used way to determine the value of a startup.

The investors focus here is a company’s exit. For this reason, one determines a possible sales price of the company in the future. This is used to calculate a valuation after the entry of an investor or a venture capital company (post-money valuation) on the valuation date, taking into account the duration and risk of the investment.

The most important influencing factors in the VC method are the company's liquidity needs, the return expected by the investor, and the time until the exit. These are used to calculate the expected enterprise value at the time of exit. The sales price on the valuation date is determined using the multiplier method. Key figures from the business plan and empirical values of comparable companies are used for this purpose.

Example: A startup in the software as a service (SaaS) sector has a liquidity need of EUR 1 million. In five years, it plans to generate revenue of EUR 5 million and record earnings before interest and tax (EBIT) in sum of EUR 1.25 million. In this case, the industry standard multiplier is 2.5x sales or 10x EBIT.

The VC investor expects a 25% return on investment on this sum and anticipates an exit in five years. The targeted exit proceeds, meaning the value of the company at a sale in five years, are calculated as follows:

Revenue x revenue multiplier = exit proceeds

EUR 5 million x 2.5 = EUR 12.5 million

The startup is worth EUR 12.5 million after five years. The future value of the investment is calculated as follows:

Liquidity need x expected return = future investment value

EUR 1 million x 1.255 = approx. EUR 3.05 million

The investor thus expects his investment of EUR 1 million to be worth EUR 3.05 million after five years. Next, the value of the investment is calculated in relation to the exit proceeds (also known as participation rate). It is assumed that the shares will not be diluted by the entry of additional investors. The formula is:

(Future investment value x 100) / exit proceeds = participation rate

(EUR 3.05 million x 100) / EUR 12.5 million = 24.4%

The future value of the investment thus amounts to 24.4% of the future company value of EUR 12.5 million. In order to determine the post-money valuation, one calculates the total enterprise value as of the calculation date using a three-price rule based on the amount of the investment:

(Liquidity need / participation rate) x 100 = post-money valuation

(EUR 1 million / 24.4%) x 100 = approx. EUR 4.098 million

The company valuation on the day of reporting thus is EUR 4.098 million (post-money). Deducting the investment in sum of EUR 1 million, one arrives at a pre-money valuation of EUR 3.098 million.

The advantage of the VC method is its quick and easy application. In addition, it requires no detailed forecast of the future development of the company. The disadvantage, however, is that the procedure only provides vague initial ideas of values and neglects specific company information. Another disadvantage is the use of multipliers. These generally refer to comparable exits in the past but are applied to an exit in the future.

Checklist Method

The checklist method considers the startup according to predefined criteria, which are weighted differently. Each venture capitalist has different criteria to which he or she pays attention, but some characteristics come up repeatedly. Among other things, the following points are dealt with in the checklist method:

- Team: Do the founders have sufficient experience in their field? Do you have management experience? Have they already founded before?

- Product: What is the unique selling point of the product? Is the product protected by trademark law?

- Market: How strong is the competitive situation on the market? How high are the entry barriers (e. g. costs for research & development, bureaucratic effort, etc.)?

- Potential: What are the chances of success for the startup? How likely is it that the product will conquer the market? What is the growth potential?

- Scalability: Can the business model be extended to other markets with little financial effort?

- Profitability: Is it possible to monetize the business idea well? Will the business model make enough profit in the future to sustain the company?

- Sustainability: Can the business model function in the long term and with changing market conditions? Are there potential developments that endanger the business model?

- Financial market: What are the capital market data (rate of charge, risk-free investments, and financial market development)? Under what conditions can the company provide itself with capital on the market?

Equidam Method

The Dutch company Equidam has developed its own method for the transparent valuation of early-stage companies without significant sales. It is a mixture of different valuation methods with different weighting. Thus, both the discounted cash flow method and the venture capital method are used. On Companisto, this method was used for the company valuation of the startup golf4you. It is made up as follows:

|

Method |

Weight |

|

The Scorecard Method |

19% |

|

The Checklist Method |

35% |

|

Venture Capital Method |

18% |

|

Discounted Cash Flow Method |

17% |

|

Discounted Cash Flow with Multiples |

11% |

Company valuation at Companisto

As an equity crowdfunding platform, Companisto is in a triangular relationship with investors and founders. While investors aim for the most affordable possible entry into the startup, i.e. a low company valuation, founders want to sell as few shares of their company as possible, i.e. a high company valuation. As the mediating party, Companisto always takes heed to protect the interests of both parties.

In the case of company valuation, however, Companisto is more likely to represent the investors’ interests. We strive to make the Companists as attractive an offer as possible. That is why we aim for lower valuations in our negotiations with startups. Ultimately, the stated valuation is the result of extensive negotiation.

During the negotiations, we also pay attention to the level of participation offered. It should be high enough to be interesting to the Companists. However, it should not be too high so as to provide little room for later investors. The participation offered should be between 5 and 20 percent.

The company valuation on Companisto serves to calculate the respective investment ratio of an investor. It is based on the startup's future expectations for economic development and earnings prospects. As these are usually early-stage investments, there is still no reliable information on sales development.

We always advise startups to estimate the projected financial figures conservatively and to build in a certain planning reserve. Future cost and margin developments should also be realistic and comprehensible. In addition, the planning premises need to be explained and match the qualitative statements of the business plan.

The company valuation does not make any statements on the existing material or asset values of the startup. It is a pure evaluation of market opportunities with high discretionary powers. The level of the company's valuation is in no way indicative of the startup's profitability or of the investment security. In the end, the Companists decide whether or not they would like to invest in the respective startup at the offered conditions.

Status as of 23.03.2017 11:14